Cloudscene’s H2, 2022 Data Center Ecosystem Leaderboard Results

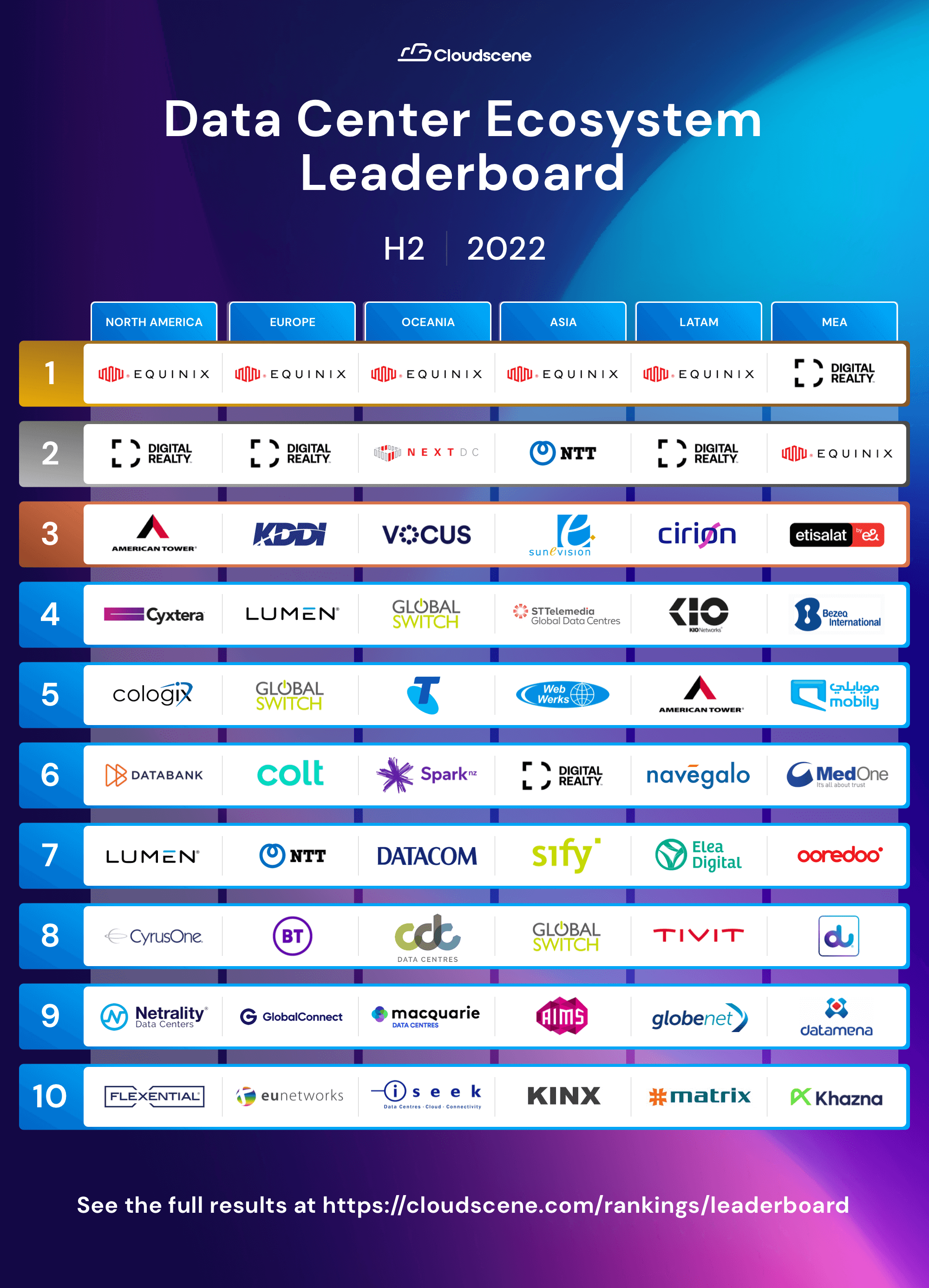

In Asia, Equinix held on to its first-place position while H1, 2022’s runner-up China Telecom slipped from the top ten. As a result, NTT Global Data Centers, SUNeVision and ST Telemedia Global Data Centres India levelled up to place second, third and fourth, respectively. An honourable mention goes to KINX for the operator’s first-time feature in Cloudscene’s Leaderboard, coming in at tenth position.

For the first time, EMEA rankings were divided to highlight the top ten data center operators in Europe and in MEA. Equinix took out first place in Europe but was surpassed by Digital Realty in the MEA region. Having placed fourth in EMEA in H1, 2022, KDDI secured a top-three spot this half-year, coming in at third in the European rankings. Etisalat, Bezeq, Mobily, MedOne, Ooredoo, du, Datamena and Khazna Data Center all made their Cloudscene Leaderboard debuts in the MEA rankings this half-year, claiming their top-ten positions among stalwart global operators.

The results for Oceania remained relatively steady, with the top three operators – Equinix, NEXTDC and Vocus Communications – retaining their respective positions from H1, 2022. Global Switch surpassed Telstra this half-year to place fourth, while Spark NZ held onto its sixth-place position. After opening a new $1.5bn data center campus in Sydney in December 2022, CDC Data Centres made its way onto the Leaderboard for the first time, coming in at eighth. iSeek also reclaimed their top-ten positioning after slipping from the rankings last half-year.

Finally, in LATAM, Equinix and Digital Realty continued their domination to secure first and second place, respectively. Claiming third place was Cirion Technologies, previously Lumen Technologies’ Latin American operations which became an independent portfolio of Stonepeak in August 2022. Other honourable mentions from the LATAM Leaderboard include KIO Networks, American Tower and Navegalo, which placed fourth, fifth and sixth, respectively.

Overall, the global network service industry underwent a period of notable growth in the second half of 2022. Europe’s domination has never been clearer with the breakdown of EMEA’s data center ecosystem results into that of Europe and MEA this half-year. The region boasts the largest global market share of service providers (45.9%) and more than half (52.7%) of network fabrics alone. Surpassed only by North America, it also has the second largest share of data centers (34.5%) and cloud on-ramps (27.7%).

North America has also retained its prominent data center footprint and performance, representing the largest percentage of data centers (35.9%) and cloud on-ramps (39.3%), and boasting an impressive 40.9% share of network fabrics and 37.1% share of service providers worldwide.

Without Europe’s contribution, MEA’s footprint and performance is relatively meagre but steadily growing. Data center providers in Oceania, Asia and LATAM are holding strong and continually contributing to a more robust data center ecosystem within their respective regions.

According to Cloudscene’s CEO, Belle Lajoie:

“The results of the H2, 2022 Leaderboard reinforce the strength of Europe and North America within the data center and IT network industry, and highlights the exciting growth potential that we are seeing in the Middle East and Africa, as well as the more developed markets of Asia and Oceania. We are looking forward to seeing how key players will continue to develop their data center ecosystems and subsequently bolster their regions’ presence and impact in the industry.”

How the H2, 2022 data was collected and calculated

Data was sourced from service providers and data center operators, and collated based on the following categories which were each assigned a weighting based on relative importance for understanding data center ecosystems across the industry:

- Total data center footprint (10%)

- Service provider ecosystem (40%)

- Total network fabric presence (10%)

- Total cloud on-ramps (40%)

For more information on our industry data and Leaderboard rankings, visit the Cloudscene Leaderboard page or get in touch with our friendly team.